You may know that I advocate frugality when it comes to investment expenses. If not, seemingly small fees compound into significant reductions in your net worth over time.

As I’ve said elsewhere, the financial services industry is a gravity machine that imperceptibly but continuously extracts fees from your pockets into a black hole of profits, bonuses, and bespoke suits.

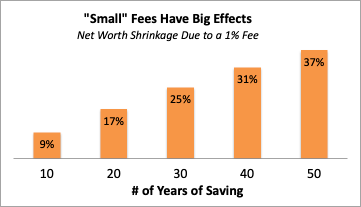

How much do these fees matter? More than you may think.

To keep it simple, let’s look at the cost of a mere 1% annual fee over various time periods:

As you can see, a 30 year span of “just” 1% fees evaporates 25% of your net worth. That’s the gravity machine at work and doesn’t seem small to me.

And, unlike nuisance fees of other industries, you’ll never even know it happened as you don’t see these investment expenses, or seemingly pay for them.

But, surely you get something for these fees? Well, no. As John Bogle (the Vanguard founder) famously quipped, “In the investment business, you get what you don’t pay for.”

On an after-fee basis, investing in low-cost index funds outperforms actively managed portfolios. The simple beauty of an index fund is that it buys the entire market and guarantees average performance at virtually no cost. As Bogle also said, “Don't look for the needle in the haystack. Just buy the haystack!”

Of course, some managers outperform the market some of the time but it won’t be the same ones each year. Over time, the financial drag of their fees will cause them to underperform.

Burt Malkiel, the author of the classic investing book, A Random Walk Down Wall Street said it another way, “A blindfolded chimpanzee throwing darts… can select a portfolio that performs as well as those managed by the experts.”

When it comes to your life savings, be cheap. Invest in low-cost index funds and you’ll have more wealth at retirement time.